Stablecoin Cards: Replatforming the $20 Trillion Payments Ecosystem

October 24, 2025

Card payments are quietly moving onto stablecoin rails, and it could be one of the biggest shifts in modern finance.

For consumers, almost nothing changes: you still tap or swipe. Your card still works everywhere Visa and Mastercard are accepted. But beneath the surface, the financial plumbing is being rebuilt on programmable, instant-settlement infrastructure.

This quiet replatforming could open the door to an entirely new class of neobanks, issuers, processors, and settlement networks, transforming how trillions of dollars flow through the global payments system.

A Massive Market Ripe for Reinvention

The global card industry represents one of the most profitable and entrenched financial ecosystems ever created. Beyond China, two networks, Visa and Mastercard, control the vast majority of the market, facilitating billions of cards and trillions in annual transaction volume.

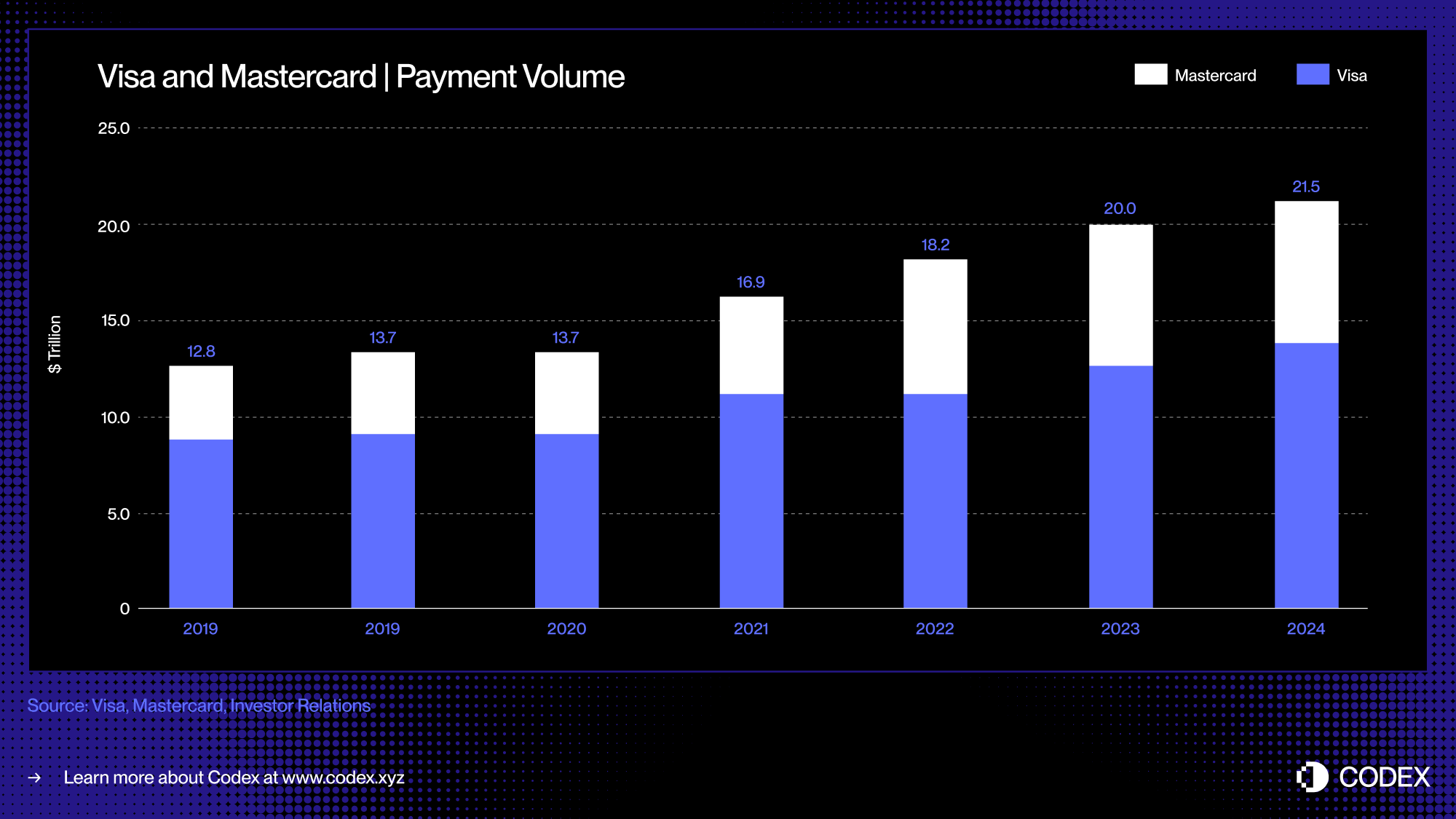

In 2024, consumers and businesses spent $13.4 trillion with Visa and $8.0 trillion with Mastercard.

There were 4.4 billion Visa and 3.2 billion Mastercard cards in circulation, with more than half issued outside the U.S., Europe, and Canada.

Visa generated $36.8 billion in revenue and $20 billion in net income, while Mastercard earned $28.2 billion and $12.9 billion, respectively.

Visa and Mastercard rank among the world’s most valuable financial institutions, with market capitalizations of approximately $665 billion and $516 billion, respectively.

Yet despite their scale, these networks remain anchored to traditional banking rails for clearing and settlement. In 2024, Visa processed just $100 million in USDC settlement volume, a rounding error in a $21 trillion market.

Moving even 1% of global card payments onto stablecoin rails would represent more than $200 billion in annual stablecoin volume, a transformative opportunity for the next generation of payment infrastructure.

How Stablecoin Cards Work

The cardholder experience remains largely unchanged, but the financial infrastructure beneath it is being rebuilt. Because shifting consumer and merchant behavior is inherently difficult, stablecoin cards provide a practical bridge, offering a seamless transition onto stablecoin rails.

The key difference lies in what powers the card. Instead of holding balances in traditional bank accounts, users hold stablecoins directly in onchain wallets. These balances can be spent anywhere Visa or Mastercard are accepted.

From the outside, nothing feels different. Cardholders still tap, swipe, or pay online as usual. Merchants still receive payments in their preferred currency. But beneath the surface, transactions clear and settle in stablecoins, enabling instant, transparent, and programmable movement of value that traditional systems simply can’t match.

Purchase: A cardholder taps or swipes their card at a merchant’s terminal. Visa and Mastercard cards are accepted by millions of merchants in over 200 countries around the globe.

Authorization: The merchant’s acquirer routes the request through the card network (Visa or Mastercard) to the card issuer, who authorizes or declines the transaction.

Clearing: At the end of the day, the card network calculates the net positions: how much each issuer owes each acquirer.

Settlement: Here’s where things change. Instead of moving money through fiat rails, settlement occurs in stablecoins. The issuer sends Visa or Mastercard the owed amount in USDC (or another stablecoin), completing the process onchain.

In many cases, the conversion from stablecoin to fiat still occurs at the point of sale. But increasingly, stablecoin-native processors can handle the entire flow end-to-end, paving the way for a fully onchain card ecosystem.

Opportunities for New Entrants

The replatforming of card payments gives rise to entirely new business models and shifts competitive advantage across the payment value chain.

Issuing Stablecoin Cards: Traditionally, the largest card issuers have been banks, Chase, Citi, Bank of America, Capital One, with a handful of fintech entrants like Nubank, Cash App, and Revolut joining the ranks.

Stablecoin cards could change this dynamic. New onchain-native issuers, or stablecoin-native neobanks, will emerge, offering consumers and businesses cards directly linked to stablecoin balances or wallets.

Processing Stablecoin Cards: Incumbent processors such as Fiserv, FIS, and TSYS serve major banks, while Marqeta built a billion-dollar business powering fintech cards for players like Cash App, Affirm and Klarna.

Now, a new class of stablecoin-native processors, such as Rain and Reap, is emerging to serve onchain issuers with programmable settlement, wallet connectivity, and composable financial logic.

On-Chain FX Protocols: As discussed in our recent analysis, onchain FX is essential to the global expansion of stablecoin payments.

In the traditional model, small issuers rely on Visa or Mastercard to handle currency conversion. Onchain FX protocols can perform this function directly between stablecoin pairs (e.g., USDC/EURC), creating an open, transparent, and efficient FX layer for card payments.

Settlement Chains: Finally, performance matters. As more issuers settle transactions in stablecoins, the settlement layer itself must deliver high throughput, predictable costs, and regulatory-grade compliance.

Purpose-built settlement chains, like Codex Chain, designed specifically for stablecoin performance and compliance, will play a central role in scaling this ecosystem.

Where Do We Go From Here?

The $20 trillion card industry won’t move onchain overnight, but the shift has already begun. As stablecoins evolve from a niche asset class into a foundational payments medium, cards represent the most practical bridge between traditional rails and the stablecoin economy.

To enable this transition, the world needs purpose-built infrastructure. Codex is designed to power that change:

Codex Chain is a settlement layer purpose-built for stablecoins. It delivers predictable transaction costs, instant settlement, and embedded compliance, creating the foundation for onchain payment networks that can match the scale and reliability of card systems.

Complementing this core technology, Codex Avenue is a global liquidity and FX hub that connects onchain and real economies. It simplifies local on/offramp, as well as stablecoin swaps, enabling frictionless movement between stablecoins and fiat across markets and currencies.

Together with our network of partners in issuance, custody, and compliance, Codex is building the stablecoin infrastructure layer for the next generation of stablecoin payments.

The stable door is open. The question is: what will you build on the other side? Let’s chat: info@codex.xyz.