The Battle for Checkout

November 7, 2025

Stablecoins are gaining traction in cross-border transfers, onchain finance, and corporate treasury. But one market remains stubbornly resistant: commerce. Despite widespread frustration with card fees and growing adoption of digital wallets, stablecoins have yet to break meaningfully into everyday consumer payments.

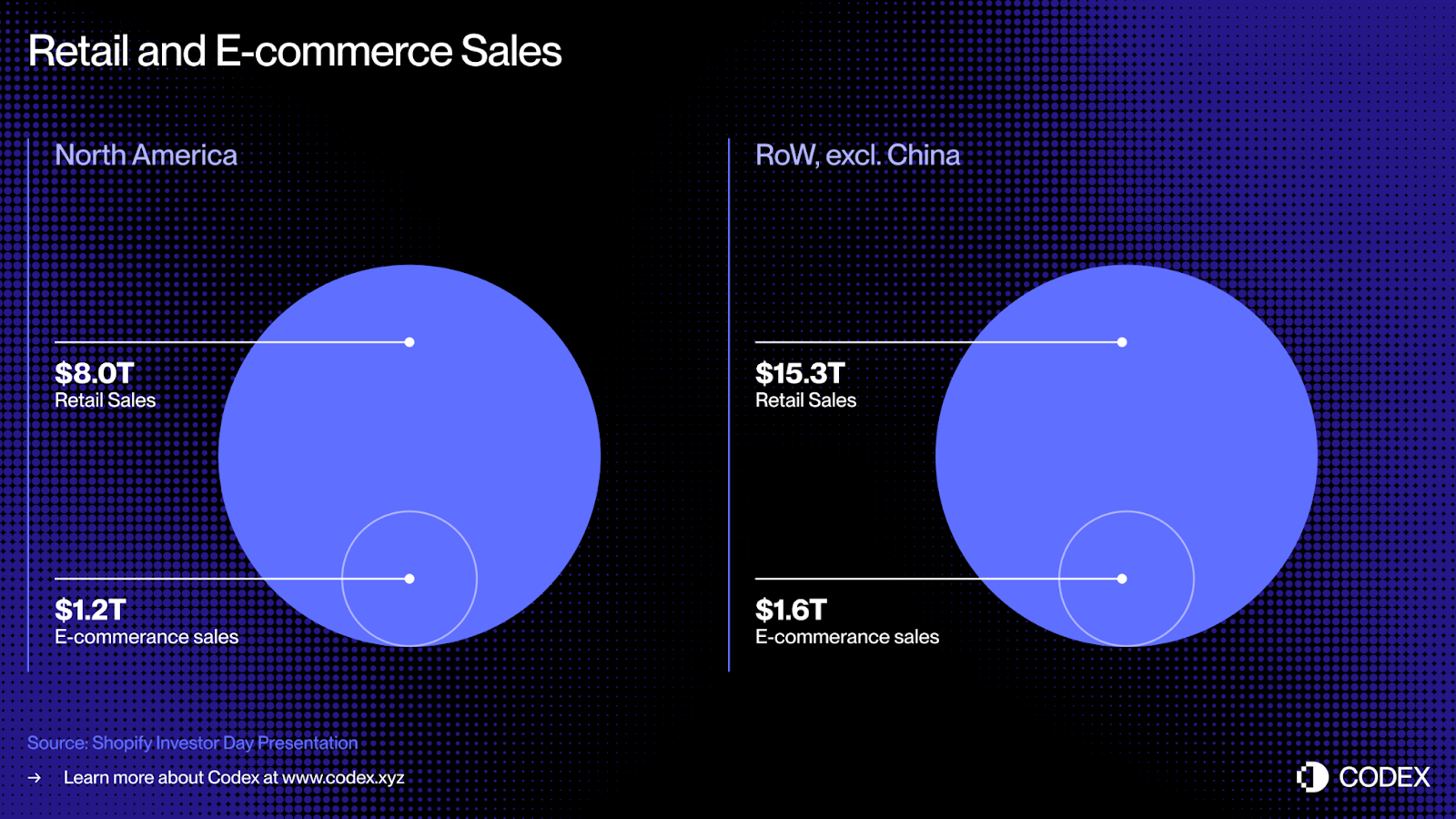

The opportunity is enormous. In the United States alone, e-commerce sales reached $1.2 trillion, and total retail sales exceeded $8 trillion. Globally, the figures are even more staggering: $1.6 trillion in e-commerce and $15.3 trillion in total retail sales. Even a single-digit shift toward stablecoin-powered payments would reshape the economics of the global payments industry.

So why hasn’t it happened yet?

Why Cards Continue to Dominate Commerce

Card networks have spent decades building the world’s most powerful consumer payment infrastructure, strengthened by a deep network effect: more consumers lead to more merchants accepting cards, which encourages more banks to issue them, which in turn drives even more usage. Over time, this flywheel has become a durable moat. Their advantage rests on four reinforcing pillars:

- Global acceptance: Everywhere you go, online or offline, cards “just work.” The acceptance footprint remains unmatched.

- Incentivized distribution: Interchange, or the fee paid by merchants to card issuers, creates powerful economic incentives for banks to issue cards and promote usage. This is how the networks gained billions of consumers.

- Embedded consumer protection: Chargebacks give consumers confidence to transact. Merchants dislike them, as they create operational complexity and cost, but the protection drives usage.

- Deep technical integrations: From point-of-sale hardware to acquirer gateways, the ecosystem is optimized for card flows. Switching is costly.

Even Apple Pay, arguably the most meaningful UX leap in consumer payments, scaled rapidly by working within the existing card infrastructure. It made cards easier to use, not fundamentally different. That’s the lesson.

When Wallets Become the New Cards

A new generation of payment instruments has quietly built distribution at a massive scale: digital wallets with hundreds of millions of users, sitting directly in the purchase flow. For the first time, we have wallet ecosystems with enough reach, trust, and daily engagement to serve as a true alternative to payment cards:

- Apple Pay (500+ million users): A universal mobile wallet embedded into every iPhone, enabling tap-to-pay, in-app purchases, and one-click online checkout with unmatched global reach.

- PayPal (400+ million users): The original internet wallet, designed for online payments and cross-border commerce, now deeply integrated into merchant checkout flows worldwide.

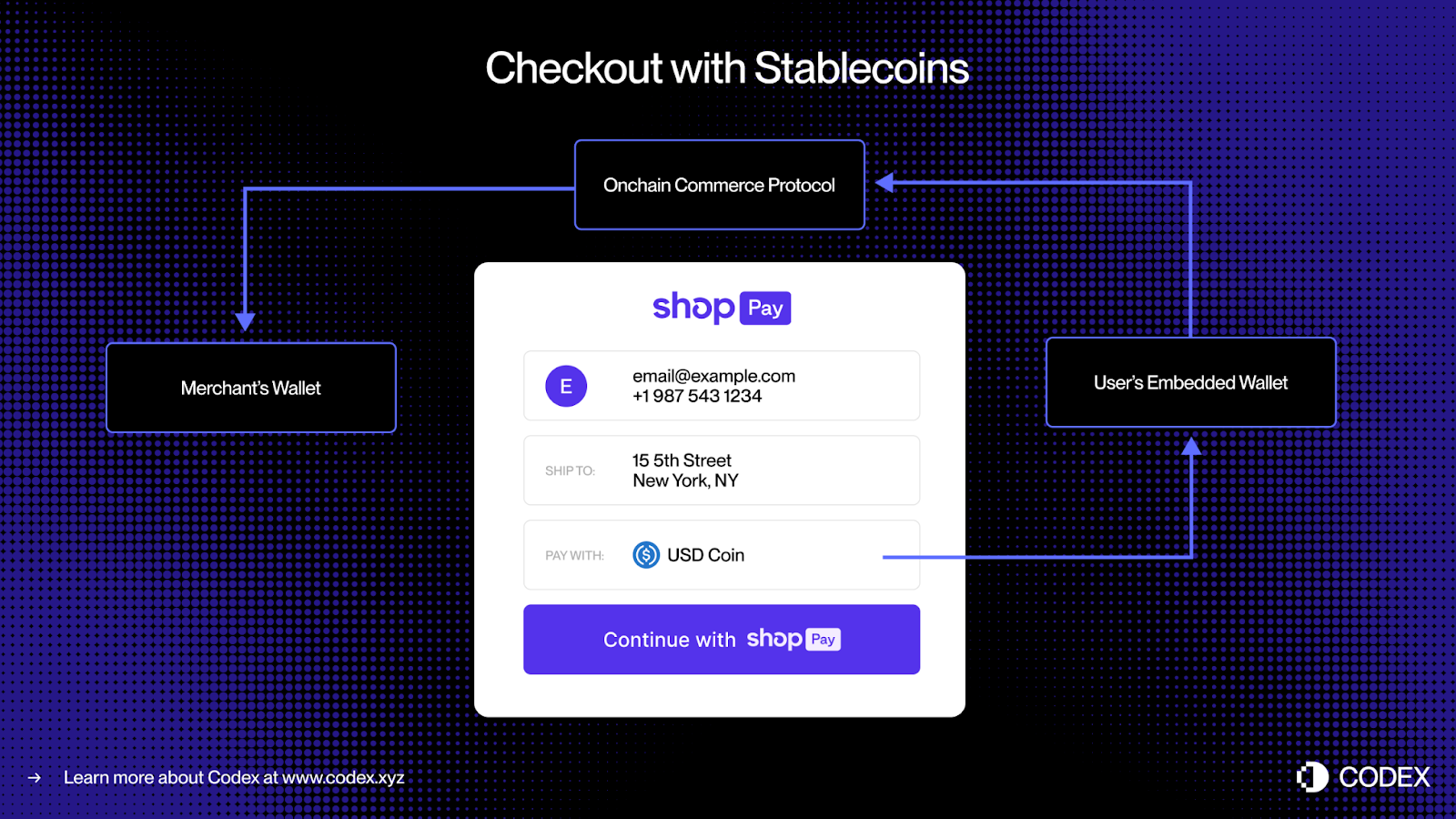

- Shop Pay and Stripe Link (hundreds of millions of users): Merchant-side checkout layers that save consumer credentials and offer one-tap payment across thousands of stores, dramatically reducing friction for both buyers and sellers.

- Affirm, Klarna, Afterpay (tens of millions of users): Credit-first wallets that sit directly in the purchase flow, combining financing, checkout, and loyalty into a single consumer experience.

These platforms already sit at checkout, online and, increasingly, in-store. Crucially, they all control their user experiences and have the technical capabilities to embed crypto wallets directly. Stripe even owns Privy, giving it native wallet-infrastructure capabilities.

The distribution exists. The UX capabilities exist. The wallets exist. So what is missing?

What’s There and What’s Still Missing

The foundations for stablecoin-powered commerce are taking shape, but key gaps remain, from offline acceptance to wallet funding, consumer protection, and incentive alignment. Online payments and wallet distribution are largely in place, yet the last mile of credit, trust, and economics still needs to be rebuilt for stablecoins to compete at scale.

- Merchant Acceptance: Online acceptance is essentially solved. Offline is improving, with early pilots from Klarna and Adyen showing promise, but wallet acceptance in in-person commerce isn’t yet as seamless as tapping a card.

- Wallet Funding Without Cards: Funding digital wallets is still the biggest bottleneck. Today, wallets are almost always topped up with cards or pre-funded balances. To truly rival card-based payments, platforms need to replicate the instant liquidity of a credit card, essentially building a credit-wallet, not just a prefunded crypto wallet.

- Consumer Protection: Chargebacks remain essential for commerce. Coinbase’s Commerce Protocol introduced important improvements, like authorization and capture flows, but a full re-imagining of consumer protection onchain is still needed.

- Incentives and Economics: Stripe and PayPal act as acquirers. With stablecoins, they no longer pay interchange and can earn yield on proprietary stablecoins, unlocking margin that can be shared with consumers via rewards or discounts. This is the first real economic wedge stablecoins can use to compete.

Where the Opportunities Are

There is still significant work ahead, across chains, protocols, wallets, acquirers, and merchants—but the prize is enormous: a modern, programmable payment rail that can compete with cards at global scale. Unlocking this opportunity will require coordinated innovation across several layers of the stack.

- Blockchains Purpose-Built for Stablecoins: Commerce payments are the most demanding category. They require high throughput, predictable fees, low latency, and atomicity. Purpose-built chains, optimized for consumer payments and merchant settlement, will become a foundational layer.

- Commerce Protocols: Chargebacks, refunds, cancellations, payment metadata, these workflows define the commerce UX. Coinbase Commerce Protocol took the first step, but a full suite of onchain commerce primitives still needs to be developed and tested.

- Loyalty, Reimagined: Stablecoins unlock a new generation of programmable loyalty, enabling real-time cash-back at checkout, onchain merchant-specific rewards, and composable programs that work across entire ecosystems.

- Payment Wallets That Compete with Cards: Cards are a magical invention - universally accepted, simple, and reliable. For wallets to compete, they must match this experience while improving on economics, speed, and interoperability.

Apple Pay showed the playbook: win through UX, preserve incentives, and leverage existing merchant integrations. Stablecoin wallets that follow this approach can scale.

The race is on, and the winners will rewrite how the world pays.